Top Earners Struggle with Credit Card and Car Debt

Rising Financial Struggles Among Upper-Income Americans

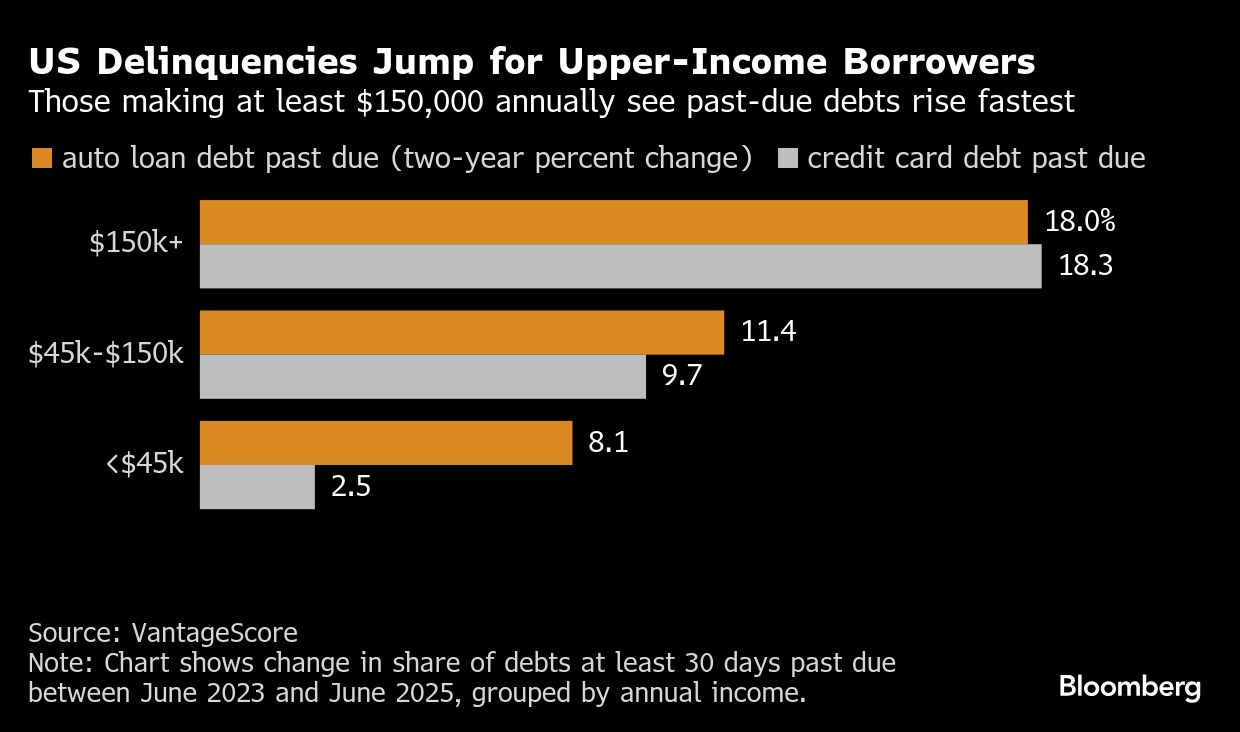

A growing trend is emerging among upper-income Americans, who are increasingly struggling to keep up with their credit card and auto loan payments. This shift highlights a deeper vulnerability in the U.S. economy as the labor market shows signs of slowing down. According to data from VantageScore, delinquencies on these types of debts have risen by nearly 20% over the past two years for individuals earning at least $150,000 annually. This increase is occurring at a faster rate than for those in middle- and lower-income brackets.

Recent studies from the Federal Reserve Bank of St. Louis show that the percentage of people making late credit card payments in the highest-income zip codes has increased twice as much over the last year compared to the lowest-income areas. These trends suggest that financial stress is not limited to any specific income group but is becoming more widespread across all levels of society.

The economic slowdown has particularly affected white-collar workers, who have seen hiring rates drop significantly. This has raised concerns about the reliance of the U.S. economy on consumer spending from top earners to sustain growth. Mark Zandi, chief economist at Moody’s Analytics, noted that financial stress is evident across all income levels. With the Federal Reserve maintaining high interest rates and the end of pandemic-era student loan forbearance programs, many individuals are finding it challenging to manage their finances.

Political Tensions and Economic Concerns

Borrowing costs have become a central issue in American politics this year, with former President Donald Trump frequently criticizing the Federal Reserve and threatening to fire its chair, Jerome Powell, for not lowering interest rates. Despite these pressures, the Fed is expected to maintain its benchmark rate unchanged during its July meeting. The central bank has kept rates high over the past two years to bring inflation back to its 2% target following a post-pandemic surge.

Concerns about Trump’s tariffs, which could drive up prices, have further delayed potential rate cuts in 2025. This uncertainty has also worsened the outlook for hiring, adding to the challenges faced by the labor market.

Personal Stories of Financial Struggle

In Brooksville, Florida, Christopher Lawton and his wife are dealing with significant debt after losing their jobs in 2023 and 2024. Their annual income dropped by around $40,000, making it difficult to cover everyday expenses. They have had to skip credit-card bills while managing auto-loan payments. The couple has started a debt-consolidation process and made efforts to reduce their expenses by canceling subscriptions and delaying non-essential purchases.

Improving job prospects has become increasingly difficult, especially for those in white-collar industries where hiring has nearly come to a standstill. A New York Fed survey shows that the perceived probability of finding a new job has been declining among higher-income individuals since 2023, now hovering just above a 50-50 chance.

Impact on Housing and Consumer Spending

High interest rates have also affected the housing market, a point that Trump has emphasized in his criticisms of the Fed. While consumers have generally managed to keep up with mortgage payments better than with credit cards and auto loans, spending on other goods and services is being squeezed.

Badri Tiwari and his wife relocated to Phoenix in 2023 with the expectation of refinancing their home when rates dropped. However, they are still waiting, and their optimism has faded. Meanwhile, Megan Locker, who works in real estate in New Hampshire, bought a home in 2020 when interest rates were low. However, her desire to make up for lost time after pandemic restrictions led to significant credit-card debt, which she and her husband are now working to pay down.

Economic Outlook and Debt Trends

Consumer spending in the first quarter of 2025 was the weakest since the onset of the pandemic, and recent data indicates ongoing caution in discretionary categories such as recreation and travel. These trends suggest that the post-pandemic model of economic growth, driven by upper-income spending on big-ticket items, is under strain.

Despite rising debt delinquencies, overall household debt levels have decreased relative to the size of the economy. In the first quarter of 2025, household debt stood at about 68% of GDP, compared to a record 98% in 2008. However, this level is still below the peak seen in previous decades, reflecting long-term changes in consumer behavior and economic conditions.

Student loans remain a significant category of household debt that has seen less deleveraging since 2008. The resumption of federal student loan payments has added to consumer stress, with the percentage of balances at least 90 days delinquent rising to 7.7% in the first quarter of 2025.

While the stock market has returned to record highs, the slow pace of hiring and limited wage growth continue to pose challenges for consumer spending. Economists warn that this financial vulnerability makes the economy more susceptible to shocks, as many individuals may not have access to credit to cushion against unexpected events.

{kind=link}

Posting Komentar untuk "Top Earners Struggle with Credit Card and Car Debt"

Posting Komentar