BEAM's Q2 Loss Shrink, Revenues Fall Short

Beam Therapeutics Reports Q2 Earnings and Pipeline Updates

Beam Therapeutics reported a loss of $1.00 per share for the second quarter of 2025, which was better than the Zacks Consensus Estimate of a $1.04 loss. This marks an improvement from the previous year's loss of $1.11 per share. However, the company’s total revenues, which include license and collaboration income, came in at $8.5 million, falling short of the expected $14 million and down from $11.8 million in the same period last year.

Despite the revenue shortfall, Beam Therapeutics continues to invest heavily in its research and development efforts. The company spent $101.8 million on R&D during the quarter, reflecting a 17% increase compared to the year-ago period. General and administrative expenses decreased by approximately 9.1% to $26.9 million.

As of June 30, 2025, the company held $1.2 billion in cash, cash equivalents, and marketable securities, with the same amount recorded as of March 31, 2025. Beam Therapeutics expects its current cash reserves to support its operations through 2028.

Pipeline Developments

The company is advancing several key candidates in its pipeline. BEAM-101, its leading ex-vivo genome-editing therapy, is being tested in the phase I/II BEACON study for adult patients with sickle cell disease (SCD). Enrollment has been completed for both adult and adolescent cohorts, with updated data expected by the end of 2025. In June, the FDA granted orphan drug designation to BEAM-101 for the treatment of SCD.

In addition to BEAM-101, Beam Therapeutics is developing BEAM-301 and BEAM-302 for glycogen storage disease type 1a (GSD1a) and alpha-1 antitrypsin deficiency (AATD), respectively. Dosing is ongoing in a phase I/II trial for BEAM-301 in the U.S., while BEAM-302 is being evaluated in a dose-escalation study for AATD. Currently, there are no approved curative treatments for AATD.

Recent results from a phase I/II study of BEAM-302 showed positive safety and efficacy data. The study is divided into two parts: Part A focuses on AATD patients with lung disease, while Part B targets those with mild-to-moderate liver disease with or without lung disease. Management recently announced that enrollment in Part B has begun, and additional doses are being explored in Part A.

As of August 1, 2025, 17 patients had been dosed in Part A of the BEAM-302 study. Treatment with BEAM-302 has shown durable correction of the disease-causing mutation and restoration of AAT physiology, with a favorable safety profile. Updated data from both parts of the study and the clinical development plan for BEAM-302 are expected in early 2026.

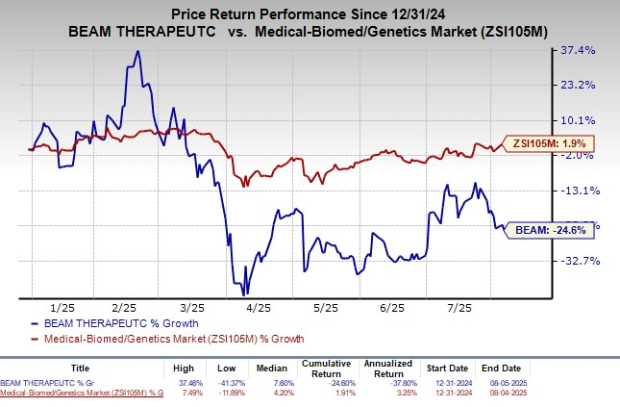

Stock Performance and Analyst Outlook

Beam Therapeutics has underperformed the broader biotech sector this year, with shares declining by 24.6% compared to the industry’s 1.9% rise. The company currently holds a Zacks Rank of #4, indicating a "Sell" rating.

Investors looking for stronger-performing biotech stocks may consider CorMedix (CRMD), Arvinas (ARVN), and Immunocore (IMCR), all of which carry a Zacks Rank of #1, or "Strong Buy." These companies have seen improved earnings estimates and positive stock performance over the past 60 days.

CorMedix has seen its 2025 EPS estimates rise from 93 cents to 97 cents, while shares have gained 48.8% year to date. Arvinas has experienced a decline of 60.3%, but its earnings have consistently beaten expectations. Immunocore has seen its 2025 loss per share estimates narrow from 86 cents to 68 cents, with a 10.2% gain in stock price.

Each of these companies has demonstrated strong earnings surprises in recent quarters, offering potential opportunities for investors seeking growth in the biotech space.

{kind=link}

Posting Komentar untuk "BEAM's Q2 Loss Shrink, Revenues Fall Short"

Posting Komentar