BMY Stock Near 52-Week Low: Buy or Sell?

Bristol Myers Squibb's Stock Performance and Strategic Moves

Bristol Myers Squibb (BMY) experienced a significant drop in its share price, hitting a 52-week low of $42.96 on July 31 following the release of its second-quarter earnings report. Despite this, the stock has since rebounded by 6.7%, currently trading at $45.85. While the company exceeded expectations in both earnings and sales for the quarter and raised its annual revenue forecast, it also revised its earnings guidance downward.

The company increased its 2025 revenue guidance to between $46.5 billion and $47.5 billion, up from $45.8 billion to $46.8 billion. This adjustment was driven by strong performance from the Growth Portfolio, improved sales from the Legacy Portfolio, and a favorable foreign exchange impact of approximately $200 million. However, BMY now anticipates adjusted earnings per share (EPS) to be in the range of $6.35 to $6.65, down from its previous guidance of $6.70 to $7. The reduction in guidance is primarily due to an unfavorable impact of 57 cents per share related to the acquired IPRD charge from the BioNTech (BNTX) deal.

Investors reacted negatively to the lowered guidance, causing the stock to decline after the announcement. To evaluate whether BMY remains a viable investment, it’s essential to examine its fundamentals and strategic initiatives.

Growth Portfolio Maintains Strong Momentum

BMY’s Growth Portfolio includes key drugs such as Opdivo, Opdivo Qvantig, Orencia, Yervoy, Reblozyl, Camzyos, Breyanzi, Opdualag, Zeposia, Abecma, Sotyku, Krazati, and Cobenfy. Revenue from this portfolio reached $6.6 billion in the second quarter, reflecting an 18% increase compared to the same period last year. This growth was largely attributed to demand for Opdivo, Breyanzi, Reblozyl, and Camzyos.

Opdivo sales in the U.S. are being driven by a successful launch in MSI-high colorectal cancer and continued growth in first-line non-small cell lung cancer. Outside the U.S., sales are fueled by volume growth. The FDA approved Opdivo Qvantig for subcutaneous use, and initial uptake has been positive across all indicated tumor types.

BMY expects global Opdivo sales, combined with Qvantig, to show mid to high single-digit growth for the full year, supported by strong performance in the first half. Reblozyl, a thalassemia drug developed in collaboration with Merck (MRK), has generated over $1 billion in global sales year-to-date. Breyanzi sales surged 125% to $344 million, while Camzyos sales jumped 87% due to robust demand.

Cobenfy, a new oral medication for schizophrenia, was approved under the brand name KarXT and represents a groundbreaking approach to treating the condition. Sales of $62 million have already been recorded, and the drug is expected to contribute significantly to BMY’s revenue in the coming years as the company expands its label into additional indications.

Decline in Legacy Portfolio Sales

The Legacy Portfolio continues to face challenges, with sales declining by 14% to $5.67 billion. This decline is due to the impact of generic competition on drugs like Revlimid, Pomalyst, Sprycel, and Abraxane, as well as changes in the U.S. Medicare Part D program. Eliquis, a blood thinner co-developed with Pfizer (PFE), remains a top performer, with global sales rising 8% due to strong demand.

Despite these challenges, BMY now expects the Legacy Portfolio to decline by 15% to 17% in 2025, a slightly more moderate rate than previously anticipated. This projection is partly due to Revlimid’s strong performance year-to-date.

Strategic Collaborations and Pipeline Expansion

BMY has made several strategic moves to strengthen its pipeline. The company recently entered into a collaboration with BioNTech to co-develop and co-commercialize BNT327, a next-generation bispecific antibody targeting PD-L1 and VEGF-A for various solid tumors. This partnership aligns with the growing interest in bispecific antibodies in cancer treatment.

In June 2025, BMY’s RayzeBio subsidiary acquired exclusive rights to OncoACP3, a prostate cancer therapeutic and diagnostic agent, from Philogen Group. Additionally, BMY partnered with Bain Capital to create a new biopharmaceutical company focused on autoimmune disease therapies. Bain Capital will invest $300 million, while BMY will license five immunology candidates.

Stock Valuation and Investment Outlook

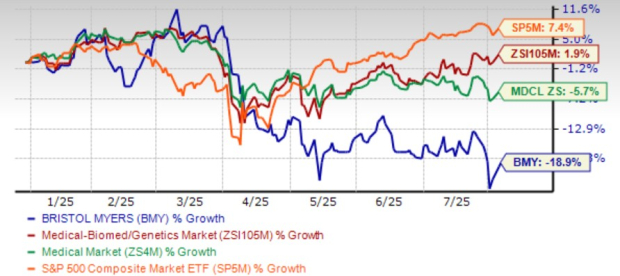

BMY’s stock has underperformed relative to the industry and the broader market, losing 18.9% year to date compared to the industry’s 1.9% growth. The stock currently trades at a forward P/E ratio of 7.48, lower than its historical average of 8.50 and the large-cap pharmaceutical industry’s 14.46. This suggests that BMY may be undervalued.

The Zacks Consensus Estimate for 2025 EPS has risen to $6.39 from $6.28, while the 2026 estimate has increased to $6.08 from $6.02. These revisions indicate some optimism about the company’s future performance.

Conclusion: A Hold for Now

BMY remains one of the largest biotech companies and is often considered a safe haven for investors in the sector. The company has shown resilience with its Growth Portfolio drugs stabilizing revenue amid generic competition. New drug approvals and label expansions could further diversify its pipeline.

However, generic competition remains a significant challenge, and new drugs may take time to offset the decline in legacy products. While BMY offers an attractive dividend yield of 5.46%, the recent earnings guidance cut and pipeline setbacks suggest that prospective investors should proceed with caution. For current holders, staying invested may still be a prudent strategy given the company’s long-term potential.

{kind=link}

Posting Komentar untuk "BMY Stock Near 52-Week Low: Buy or Sell?"

Posting Komentar