CLOV Q2 Earnings Meet Expectations, Stock Drops on Higher Insurance Risk Outlook

Clover Health Investments, Corp. Reports Second-Quarter 2025 Results

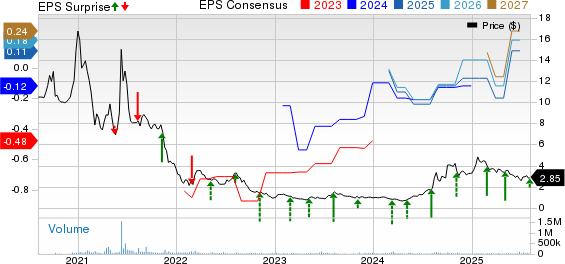

Clover Health Investments, Corp. (CLOV) reported second-quarter 2025 earnings per share (EPS) of 3 cents, which is an improvement compared to the 1 cent recorded in the same period last year. This figure met the Zacks Consensus Estimate, indicating that the company’s performance was in line with expectations.

However, when considering adjusted EPS from continuing operations, the company reported approximately 3 cents, a decline from the 7 cents recorded in the year-ago quarter. This suggests that while the bottom line was consistent with expectations, there were underlying factors affecting the adjusted results.

Revenue Growth and Performance

Clover Health generated revenues of $477.6 million during the quarter, reflecting a 34.1% increase year over year. Despite this growth, the revenue figure fell short of the Zacks Consensus Estimate by 1%. The primary driver of this revenue growth was the Insurance segment, which saw significant gains due to increased Medicare Advantage membership and improved member retention.

The Insurance segment contributed $469.8 million in revenue, up 34.3% from the previous year. Management attributed this growth to a 32% increase in Medicare Advantage membership, along with effective cohort management strategies. However, the Insurance Benefit Expense Ratio (BER) rose to 88.4%, up from 76.1% in the prior-year quarter. This increase was partially influenced by the implementation of a Clover Assistant-enabled affiliate entity.

Other income for the quarter reached $7.8 million, representing a 21.8% increase from the previous year. This growth highlights the company’s efforts to diversify its revenue streams beyond the core insurance business.

Operational Update

During the second quarter, Clover Health experienced a 52.2% year-over-year increase in net medical claims, reaching $378 million. Salaries and benefits expenses also rose by 10.5% to $61.3 million, while general and administrative expenses increased by 9.1% to $48.5 million. As a result, total operating expenses climbed to $488.2 million, marking a 39.9% increase compared to the same period last year.

The company reported an operating loss of $10.6 million for the quarter, down from an operating profit of $7.2 million in the prior-year period. This shift indicates challenges in maintaining profitability despite strong revenue growth.

Financial Position

At the end of the second quarter, Clover Health had cash and cash equivalents of $188.6 million, an increase from $155.4 million at the end of the first quarter. However, net cash used in operating activities from continuing operations was $10.9 million, compared to net cash provided by operating activities of $70.7 million in the same period last year. This change highlights the company’s ongoing cash flow challenges.

Guidance and Outlook

Clover Health has reaffirmed its sales and income outlook for 2025. The company expects Insurance revenues to range between $1.8 billion and $1.875 billion, reflecting a 37% year-over-year growth at the midpoint. Adjusted Net Income is projected to be in the range of $50 million to $70 million.

In addition, the company has raised its projection for the Insurance BER, now expected to be between 88.5% and 89.5%, up from the previous range of 87% to 88%. Average Medicare Advantage membership is also expected to increase to between 104,000 and 108,000, implying a 32% year-over-year growth.

Market Reaction and Strategic Focus

Following the release of the second-quarter results, CLOV shares fell by 15.1% during after-hours trading on August 5. The decline was attributed to lower-than-expected earnings and revenue guidance that fell below Wall Street estimates. Over the year-to-date period, the stock has lost 9.5%, underperforming the industry's 22.4% growth and the S&P 500 Index's 7.4% increase.

The drop in share price has been linked to rising medical cost ratios, particularly due to elevated Part D utilization and higher supplemental benefits costs in dental. While management reaffirmed its profitability guidance, the revised BER projection signals potential margin pressures for the remainder of 2025.

A key strategic initiative for Clover Health is its Counterpart Health initiative, which extends its technology platform to external risk-bearing entities. This program has shown encouraging uptake and is expected to support future growth.

Industry Comparison and Investment Opportunities

Clover Health currently holds a Zacks Rank of #3 (Hold). In the broader medical space, several better-ranked stocks have also announced quarterly results. These include:

- Medpace Holdings, Inc. (MEDP): Holding a Zacks Rank of #1 (Strong Buy), Medpace reported second-quarter 2025 EPS of $3.10, beating estimates by 3.3%.

- West Pharmaceutical Services, Inc. (WST): With a Zacks Rank of #1, West Pharmaceutical reported adjusted EPS of $1.84, exceeding estimates by 21.9%.

- Boston Scientific Corporation (BSX): Carrying a Zacks Rank of #2 (Buy), Boston Scientific posted adjusted EPS of 75 cents, surpassing estimates by 4.2%.

These companies demonstrate strong performance and are considered favorable investment options in the current market environment.

{kind=link}

Posting Komentar untuk "CLOV Q2 Earnings Meet Expectations, Stock Drops on Higher Insurance Risk Outlook"

Posting Komentar