ESPR Surpasses Estimates, Stock Soars in Q2

Esperion Therapeutics Reports Stronger-Than-Expected Q2 Results

Esperion Therapeutics reported better-than-expected financial results for the second quarter of 2025, with a narrower loss than anticipated. The company recorded a loss of 2 cents per share, significantly better than the Zacks Consensus Estimate of a 17-cent loss. This improvement reflects a positive shift in performance compared to the previous year, when the company had a loss of 5 cents per share (excluding the loss on extinguishment of debt).

In terms of revenue, Esperion generated total revenues of $82.4 million during the quarter, representing a 12% increase year-over-year. This figure also exceeded the Zacks Consensus Estimate of $66 million. When excluding the one-time milestone received from Daiichi Sankyo Europe (DSE) for the quarter ended June 2024, total revenues saw an impressive 69% year-over-year growth.

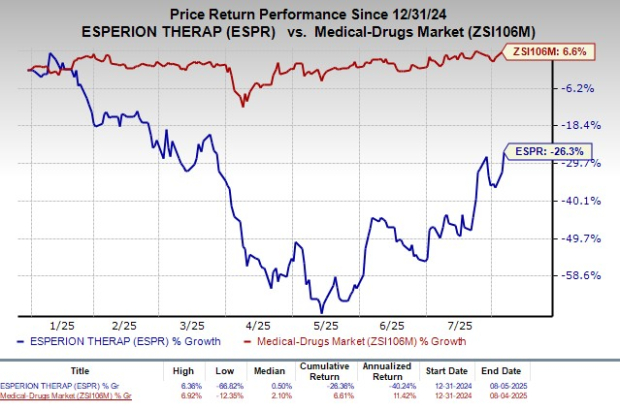

The stock of Esperion responded positively to these results, with shares rising 8.7% on August 5. Despite this gain, the stock has experienced a decline of 26.3% year-to-date, while the broader industry saw a 6.6% increase.

Key Products and Revenue Streams

Esperion’s commercial portfolio includes two FDA-approved drugs: Nexletol and Nexlizet. These oral medications are used to treat elevated LDL-C (bad cholesterol) and reduce cardiovascular risk. In the U.S., they are marketed as Nilemdo and Nustendi, while in ex-U.S. markets (excluding Japan), they are distributed through partnerships with Daiichi Sankyo. The company earns royalties on sales of its drugs in these international markets.

Nexlizet is a combination therapy consisting of bempedoic acid and ezetimibe. During the second quarter, product revenues from the United States totaled $40.3 million, a 42% increase compared to the same period last year. This outperformed the Zacks Consensus Estimate of $35.1 million.

Collaboration revenues, which include combined royalty and partner revenues, reached $42.1 million during the quarter. This represents a nearly 7% decline year-over-year, primarily due to a milestone payment recorded in the previous year. However, excluding settlement agreement milestones, collaboration revenues surged by around 105% year-over-year. These figures also surpassed the Zacks Consensus Estimate of $31.2 million and the model estimate of $35.6 million.

Operational Improvements and Financial Outlook

Research and development expenses decreased by 37% year-over-year to $7.2 million, reflecting lower costs in ongoing clinical studies. Selling, general, and administrative expenses also declined by 11% to $39.5 million, driven by reduced media and marketing expenditures.

Notably, the second quarter marked the first time in the company's history that it achieved operating income from its ongoing business operations. As of June 30, 2025, Esperion held cash, cash equivalents, restricted cash, and investment securities totaling $86.1 million, down from $114.6 million as of March 31, 2025.

Looking ahead, Esperion expects operating expenses for 2025 to range between $215 million and $235 million, including $15 million in non-cash expenses related to stock compensation. The company anticipates achieving sustainable profitability starting in the first quarter of 2026.

Recent Developments and Strategic Moves

Esperion recently entered into settlement agreements with three abbreviated new drug application (ANDA) filers regarding patents for Nexletol. Under the terms of these agreements, the ANDA filers will not be able to market a generic version of Nexletol until 2040. This move is expected to help protect the company's sales from potential generic competition in the U.S. market.

Performance and Market Position

Esperion currently holds a Zacks Rank of #3 (Hold). In comparison, several other biotech stocks have higher rankings. For instance:

- CorMedix (CRMD) has a Zacks Rank of #1 (Strong Buy), with earnings per share estimates for 2025 increasing from 93 cents to 97 cents.

- Arvinas (ARVN) also carries a Zacks Rank of #1, with 2025 loss per share estimates narrowing from $1.51 to $1.50.

- Immunocore (IMCR) maintains a Zacks Rank of #1, with 2025 loss per share estimates improving from 86 cents to 68 cents.

These companies have shown strong earnings surprises in recent quarters, indicating positive investor sentiment.

{kind=link}

Posting Komentar untuk "ESPR Surpasses Estimates, Stock Soars in Q2"

Posting Komentar