FMS Surpasses Expectations with Strong Q2 Earnings and Rising Revenues

Strong Performance in Q2 2025 for Fresenius Medical Care AG & Co.

Fresenius Medical Care AG & Co. (FMS) delivered impressive results in the second quarter of 2025, exceeding expectations across key financial metrics. The company reported adjusted earnings per share (EPS) of 52 cents, surpassing the Zacks Consensus Estimate by 4%. This marked a significant year-over-year improvement of 36.8%, highlighting the company’s strong operational performance.

Revenue Growth and Strategic Adjustments

The company’s revenue reached $5.44 billion (EUR 4,792 million), which exceeded the Zacks Consensus Estimate by 1.6%. On a year-over-year basis, revenue increased by 1% and by 5% at constant currency (cc). Additionally, the company saw a 7% organic growth, reflecting underlying demand in its core markets.

Management attributed a minor negative impact on revenue to divestitures under the portfolio optimization plan, which reduced revenue by EUR 6 million during the quarter. For the full year, these actions are expected to have a 100 basis point negative impact on top-line growth in 2024.

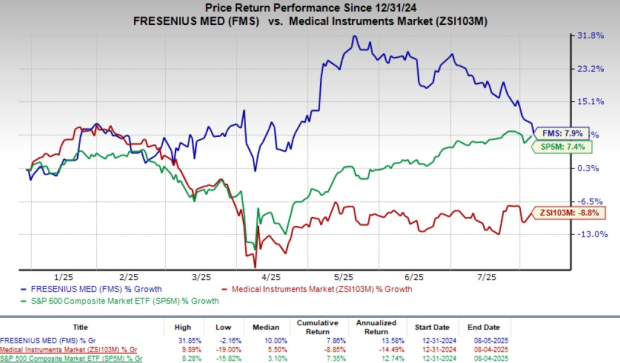

Despite these challenges, FMS shares rose nearly 2.2% in after-market trading, with the stock gaining 7.9% year-to-date compared to an industry decline of 8.8%. Meanwhile, the S&P 500 Index recorded a 7.4% increase over the same period.

Segment Performance

In 2024, Fresenius Medical restructured its operations into two new segments: Care Delivery and Care Enablement.

Care Delivery Segment

Revenues for this segment declined by 3% year-over-year but grew by 1% at constant currency. On an organic basis, revenues increased by 4%. In the U.S., market revenues fell by 2% but rose by 3% organically. Management cited unfavorable exchange rates and increased mortality due to a severe flu season as factors affecting sales. However, this was partially offset by higher patient starts, reimbursement rate increases, and a favorable payor mix.

Internationally, sales dropped by 8% overall and at constant currency, but grew by 5% organically. This growth was driven by accelerated same-market treatment growth of 1.7%, despite the impact of divestitures.

Care Enablement Segment

This segment saw a 1% decline in revenue year-over-year but experienced growth of 3% at constant currency and organically. Volume growth and positive pricing momentum were tempered by unfavorable exchange rate effects.

Financial Highlights

Gross profit improved by 4.2% year-over-year, with gross margin expanding by 90 basis points (bps) to 25.4%. Selling, general, and administrative expenses increased by 2.7% on a reported basis, while research and development expenses decreased by 17.4%.

Adjusted operating income rose by 9.2% from the prior-year quarter, with the adjusted operating margin expanding by 80 bps to 9.9%.

2025 Guidance and Strategic Initiatives

For 2025, Fresenius Medical anticipates positive revenue growth at a low-single-digit rate compared to the previous year. Operating income is expected to grow by a high-teens to high-twenties percent rate.

The company also continues to implement its FME25 transformation program, which has already generated EUR 58 million in sustainable savings. While one-time costs related to the initiative amounted to EUR 53 million, the company remains confident in achieving its full-year target of around EUR 180 million in additional annual savings by 2027.

Industry Outlook and Competitive Landscape

Fresenius Medical currently holds a Zacks Rank of #1 (Strong Buy), reflecting strong investor confidence. Several other medical sector companies have also reported robust quarterly results:

- Medpace Holdings, Inc. (MEDP): EPS of $3.10 beat estimates by 3.3%, with revenue of $603.3 million surpassing expectations by 11.5%. The company has a long-term growth rate of 11.4%.

- West Pharmaceutical Services, Inc. (WST): Adjusted EPS of $1.84 exceeded estimates by 21.9%, with revenue of $766.5 million beating expectations by 5.4%. The company has a long-term growth rate of 8.5%.

- Boston Scientific Corporation (BSX): Adjusted EPS of 75 cents surpassed estimates by 4.2%, with revenue of $5.06 billion outperforming expectations by 3.5%. The company has a long-term growth rate of 14%.

These companies, like FMS, demonstrate strong performance in the broader healthcare sector, reinforcing the potential for continued growth in the coming quarters.

{kind=link}

Posting Komentar untuk "FMS Surpasses Expectations with Strong Q2 Earnings and Rising Revenues"

Posting Komentar