Q3 Earnings and Revenues Top Expectations, EPS Forecast Upgraded

Strong Performance in Q3 Fiscal 2025

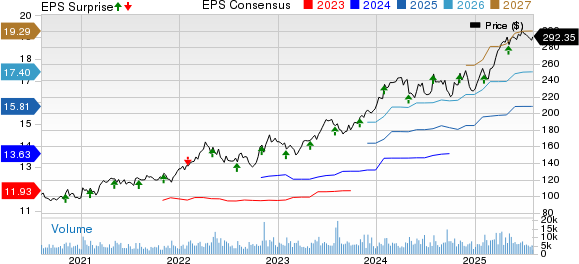

Cencora, Inc. reported strong results for the third quarter of fiscal 2025, with adjusted earnings per share (EPS) reaching $4.00, surpassing the Zacks Consensus Estimate of $3.78 by 5.8%. This marked a significant improvement of 19.8% year over year. The company also saw a notable increase in GAAP EPS, which reached $3.52, up 45.5% from the same period last year. This growth was largely attributed to strong revenue performance.

Revenue Growth and Market Performance

Revenues for the quarter totaled $80.7 billion, reflecting an 8.7% year-over-year increase. This figure slightly exceeded the Zacks Consensus Estimate by 0.5%. The company’s U.S. Healthcare Solutions segment was a key driver of this growth, reporting revenues of $72.9 billion, a rise of 8.5% compared to the previous year. This increase was fueled by market expansion and higher unit volumes, particularly in GLP-1 drugs and specialty products.

The segment's operating income reached $901.8 million, up 29.1% year over year. This growth was supported by increased product sales and the acquisition of RCA in January 2025, although it was partially offset by rising operating expenses.

In contrast, the International Healthcare Solutions segment saw revenues of $7.8 billion, a 10.5% increase year over year. At constant currency, the top line grew by 8.8%. However, operating income declined to $156.2 million, down 12.9% on a reported basis and 16.2% at constant currency. This decline was primarily due to lower operating income in global specialty logistics and consulting services businesses.

Margin Improvements and Financial Position

Cencora reported an adjusted gross profit of $2.9 billion, up 20.7% year over year. As a percentage of total revenues, the adjusted gross margin improved to 3.55%, up 36 basis points from the previous year. Adjusted operating income for the quarter was $1.1 billion, representing a 20.6% increase year over year. The adjusted operating margin expanded to 1.31%, up 13 basis points from the prior year.

Financially, Cencora ended the quarter with cash and cash equivalents totaling $2.23 billion, compared to $1.98 billion in the previous quarter. Cumulative net cash provided by operating activities amounted to $741.7 million, a decrease from $2.48 billion in the same period last year.

Dividend and Guidance Updates

The company's board of directors declared a quarterly dividend of 55 cents per share, payable on September 2, 2025, to shareholders of record as of August 15, 2025.

Cencora also updated its fiscal 2025 guidance, raising its adjusted EPS forecast to a range of $15.85–$16.00, up from the previous guidance of $15.70–$15.95. Total revenues are now expected to grow approximately 9%, compared to the earlier estimate of 8–10%. For the U.S. Healthcare Solutions segment, revenue growth is projected to be in the range of 9–10%, while the International Healthcare Solutions segment is expected to see growth between 6–7%, up from the previous guidance of 3–4%.

Adjusted operating income for the full year is now expected to improve by 15–16%, up from the earlier forecast of 13.5–15.5%. The U.S. Healthcare Solutions segment is anticipated to see a 20–21% increase in operating income, while the International Healthcare Solutions segment is expected to face a decline of around 6% year over year.

Analyst Perspective and Market Outlook

Despite the strong financial results, Cencora’s shares were down 0.8% in pre-market trading. So far this year, the stock has gained 29.4%, outperforming the industry’s decline of 3% and the S&P 500 Index, which fell 5% during the same period.

Cencora continues to benefit from robust performance across all segments, driven by strong demand for specialty products and GLP-1 drugs. The company remains focused on strategic initiatives and efficient operations. The recent acquisition of RCS is expected to positively impact the bottom line this fiscal year.

However, challenges remain, including the negative impact of lower-margin GLP-1 drugs and the absence of high-margin COVID-19 therapies. Rising operational costs amid inflationary pressures and intense competition in the MedTech sector also pose headwinds.

Zacks Rank and Other Key Stocks

Cencora currently holds a Zacks Rank #2 (Buy). Other top-ranked stocks in the medical space include:

- Medpace Holdings, Inc. (MEDP): Carries a Zacks Rank #1 (Strong Buy), with second-quarter 2025 EPS of $3.10, beating estimates by 3.3%.

- West Pharmaceutical Services, Inc. (WST): Holds a Zacks Rank #1, with second-quarter 2025 adjusted EPS of $1.84, exceeding estimates by 21.9%.

- Boston Scientific Corporation (BSX): Has a Zacks Rank #2, with second-quarter 2025 adjusted EPS of 75 cents, surpassing estimates by 4.2%.

These companies have consistently outperformed expectations in recent quarters, offering investors potential opportunities in the healthcare sector.

{kind=link}

Posting Komentar untuk "Q3 Earnings and Revenues Top Expectations, EPS Forecast Upgraded"

Posting Komentar