Vistra's Q2 Earnings Preview: What's Next for the Stock?

Overview of Vistra Corp's Second-Quarter 2025 Performance

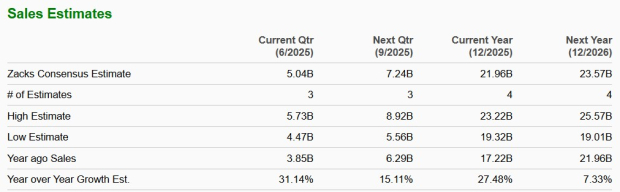

Vistra Corp is set to report its second-quarter 2025 results on August 7, before the market opens. Analysts anticipate improvements in both revenue and earnings per share for the company. The Zacks Consensus Estimate for Vistra’s second-quarter revenues stands at $5.04 billion, reflecting a significant increase of 31.14% compared to the same period last year. Additionally, the estimated earnings per share for the quarter are at 98 cents, marking an 8.89% rise from the previous year’s figure.

Historical Earnings Performance

Looking back, Vistra has shown mixed performance in its recent quarters. In one of the last four quarters, the company surpassed earnings expectations, while it met expectations once and fell short twice. On average, the earnings surprise was 58.13%, indicating some variability in its financial results.

Zacks Model Insights

According to the Zacks model, there is no definitive prediction that Vistra will beat earnings expectations this time. The combination of a positive Earnings ESP (Earnings Surprise Prediction) and a Zacks Rank of #1 (Strong Buy), #2 (Buy), or #3 (Hold) typically increases the likelihood of an earnings beat. However, in this case, the Earnings ESP for Vistra is 0.00%, and the Zacks Rank is currently #3. This suggests that while the company may not be a strong candidate for an earnings beat, investors should still monitor its performance closely.

Other Stocks to Consider

Investors might also look into other companies within the same sector that could potentially post earnings beats. For example:

- Sempra Energy (SRE): Expected to report an earnings beat with an Earnings ESP of +0.60% and a Zacks Rank of #2. Its long-term earnings growth rate is 7.94%, though the Zacks Consensus Estimate for earnings is slightly lower than the previous year.

- MDU Resources Group: Also anticipated to deliver an earnings beat, with an Earnings ESP of +20% and a Zacks Rank of #2. However, the Zacks Consensus Estimate for earnings is expected to decrease by 59.4% year-over-year.

Factors Influencing Vistra’s Q2 Earnings

Several factors are likely to have contributed to Vistra’s second-quarter performance. Increasing demand for clean electricity across its service area has been a key driver, fueled by the expansion of large U.S. data centers and the ongoing electrification of the Permian Basin. Vistra’s diversified generation portfolio, which includes a high-quality nuclear fleet, positions the company well to capitalize on this growing demand.

Additionally, Vistra’s integrated business model focuses on providing reliable and affordable electricity to customers, which supports its revenue growth. Share repurchases have also played a role in boosting shareholder value and earnings per share. From November 2021 through May 2, 2025, the company executed $5.2 billion in share repurchases, which reduced outstanding shares and increased earnings per share. Management plans to continue these buybacks, aiming to repurchase at least $1.5 billion worth of shares between 2025 and 2026.

Vistra also employs a hedging program to mitigate the impact of market changes and price fluctuations. All of its 2025 generation volume is hedged, ensuring stable generation volumes for the quarter.

Price Performance and Valuation

Vistra’s stock has outperformed the industry over the past year, gaining 173.7% compared to the industry’s 15.2% rally. However, the company is currently valued at a premium compared to its industry peers on a forward 12-month P/E basis.

Investment Thesis

Vistra is expanding its generation capacity through a mix of organic initiatives and strategic acquisitions. Its integrated business model provides a competitive edge over non-integrated competitors. However, operating nuclear power plants involves inherent risks that could affect the company’s revenue and financial performance. There are concerns about whether Vistra has sufficient insurance coverage to manage these risks effectively.

Final Thoughts

Vistra operates in a region experiencing rising demand for clean electricity. The company is actively expanding its clean energy generation capacity through acquisitions and organic growth to meet this demand. Its stable hedging strategy and growing residential customer base further strengthen its position in the market.

Despite its positive outlook, the stock is currently trading at a premium. New investors may want to consider waiting for a more attractive entry point, potentially after the release of the second-quarter earnings report.

{kind=link}

Posting Komentar untuk "Vistra's Q2 Earnings Preview: What's Next for the Stock?"

Posting Komentar