Baidu's Soaring Costs Threaten Profits: Can AI Growth Save the Day?

Baidu's Financial Struggles and Strategic Investments in AI

Baidu, Inc. (BIDU) is facing significant financial pressure as rising costs begin to erode its profits, even as the company intensifies its focus on artificial intelligence (AI). This challenge is reflected in its margins, with the cost of revenues increasing by nearly 12% year over year in the second quarter of 2025. This growth was driven by the expansion of Baidu’s AI Cloud infrastructure, while higher operating expenses further reduced operating leverage and EBITDA. Additionally, management has warned that the advertising market will remain weak in the third quarter, which limits near-term recovery opportunities.

The financial strain is becoming more apparent. Free cash flow turned negative at RMB 4.7 billion, and revenues declined by 4% year over year to RMB 32.7 billion. The core online marketing segment, which remains Baidu’s largest revenue source, dropped by 15% year over year during the reported quarter. This decline highlights the growing gap between the weakness in traditional advertising and the heavy investments in AI.

Despite these challenges, Baidu is working to lay the foundation for long-term growth. The momentum behind its AI Cloud is being driven by enterprise demand, the Ernie model, and Apollo Go’s autonomous ride services. By July, 64% of mobile searches already featured AI-generated content, showing strong user adoption even before monetization efforts began. With a substantial cash reserve of RMB 124 billion, the company has the resources to optimize GPU usage, secure domestic chip flexibility, and refine AI monetization pilots.

The broader AI market presents a favorable tailwind, with global spending projected to grow at a compound annual rate of 35.9% through 2030, reaching $1.8 trillion according to a report from Grand View Research. For Baidu, the key challenge lies in converting this adoption into profitability quickly enough to offset declines in advertising revenue. Considering these factors, the current cash constraints can be viewed as a catalyst for long-term AI-driven growth.

Global Competitors in the AI Race

Alphabet (GOOGL) faces similar pressures due to the high costs associated with scaling up its AI and cloud infrastructure. The company has committed to investing over $85 billion in AI and cloud initiatives, which is driving up operating costs but also fueling rapid growth in Google Cloud. Alphabet’s dominant ad business, extensive ecosystem, and global reach provide it with significant cash flow and data advantages that Baidu lacks. With its scale, diversified revenue streams, and ability to spread costs across various services, Alphabet maintains margin resilience. Ultimately, Alphabet’s superior resources and global dominance make it a stronger competitor in the AI race compared to Baidu.

Microsoft (MSFT) is also making massive investments in AI infrastructure, particularly in Azure data centers. The company has committed over $80 billion in fiscal 2025 for these initiatives, with additional costs expected in 2026. Microsoft benefits from its vast scale, diversified revenue streams, and partnership with OpenAI, which helps it spread expenses, optimize operations, and preserve margins. Unlike Baidu, Microsoft has a global reach, strong Azure growth, and greater efficiency in managing AI costs, making it more resilient and dominant in the AI race.

Baidu's Price Performance, Valuation, and Estimates

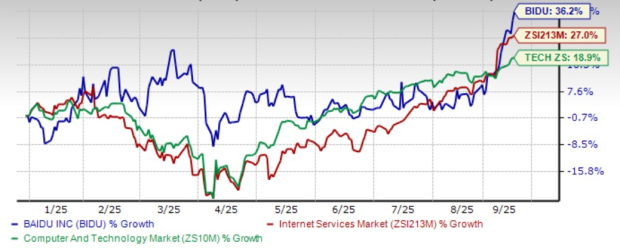

Baidu’s shares have gained 36.2% year to date, outperforming both the Zacks Internet - Services industry and the Zacks Computer and Technology sector, which saw growth of 27% and 18.9%, respectively. From a valuation standpoint, Baidu’s forward 12-month price/earnings ratio stands at 12.62, significantly below the industry average of 23.74. The company currently holds a Value Score of C.

The Zacks Consensus Estimate for full-year 2025 earnings is set at $8.32 per share, reflecting a 3.9% decrease over the past 30 days and a 20.99% year-over-year decline. Baidu currently carries a Zacks Rank of #5 (Strong Sell).

{kind=link}

Posting Komentar untuk "Baidu's Soaring Costs Threaten Profits: Can AI Growth Save the Day?"

Posting Komentar