ET Stock Surpasses Industry Gains: What's the Strategy?

Energy Transfer LP: A Strong Performer in the Oil and Gas Sector

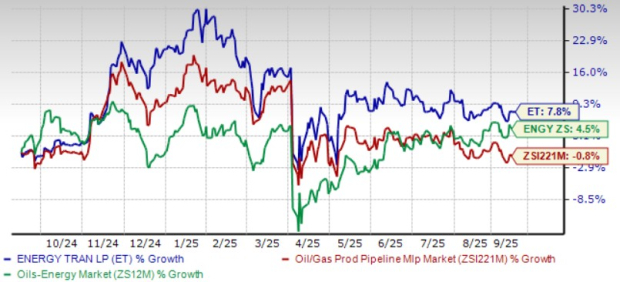

Energy Transfer LP (ET) has shown impressive performance over the past year, with its stock rising by 7.9%. This is a stark contrast to the Zacks Oil and Gas - Production Pipeline - MLB industry, which experienced a decline of 0.8% during the same period. As a midstream oil and gas company, ET operates a vast network of pipelines across the United States. The company is actively pursuing opportunities to meet the growing demand for energy from new centers within its network.

In addition to its pipeline infrastructure, ET is also a top exporter of liquefied petroleum gas. The company is investing in expanding its natural gas liquids (NGL) export facilities to meet the increasing global demand for NGL. These efforts position ET well for future growth.

Price Performance Analysis

When looking at the one-year price performance of Energy Transfer, it's clear that the company has outperformed many of its peers. The 50-day simple moving average (SMA) is currently above the stock’s price, indicating a bullish trend. This technical indicator is widely used by traders and analysts to identify potential support and resistance levels, as well as early signals of market trends.

However, should investors consider adding ET to their portfolio solely based on recent price movements? To determine whether this is a good entry point, it's essential to examine the underlying factors driving the company's growth.

Key Factors Driving Energy Transfer’s Growth

A significant portion of Energy Transfer’s revenue comes from fee-based contracts tied to its transportation and storage services. These long-term agreements with creditworthy counterparties provide stable cash flow and reduce exposure to volatile commodity prices. With U.S. oil and gas production on the rise, ET is well-positioned to benefit from increased demand for pipeline infrastructure.

The company's extensive midstream network spans nearly 140,000 miles of pipelines across North America, covering natural gas, NGLs, crude oil, and refined products. This scale and integration give ET a competitive edge, allowing it to efficiently transport volumes from major basins like the Permian, Eagle Ford, and Marcellus to key demand centers and export hubs.

Energy Transfer is also capitalizing on the rising demand for U.S. natural gas through its intrastate and interstate storage network. Strategically located along major demand corridors, these assets enhance reliability, manage seasonal fluctuations, and support peak needs. Ongoing expansion further strengthens ET’s role in balancing U.S. gas markets, supporting long-term earnings stability and growth.

Strategic Acquisitions and Investments

Energy Transfer has grown steadily through strategic acquisitions that add complementary assets and enhance its operations. Deals such as WTG Midstream, Lotus Midstream, and Crestwood Equity Partners have strengthened ET’s natural gas and NGL network while expanding its presence in high-growth basins like the Permian, Williston, and Haynesville.

In addition to acquisitions, the company is investing in high-return midstream projects to boost efficiency and expand services. In the first half of 2025, ET allocated $2.4 billion, with full-year capital spending expected to reach about $5 billion. These investments are aimed at strengthening and growing its infrastructure.

Earnings Outlook and Dividend Performance

The Zacks Consensus Estimate for Energy Transfer’s 2025 and 2026 earnings per unit indicates year-over-year growth of 8.59% and 10.91%, respectively. This positive outlook reflects the company’s strong fundamentals and growth potential.

Energy Transfer currently pays a quarterly cash distribution of 33 cents per common unit. Management has raised distribution rates 16 times in the past five years, with a current payout ratio of 102%. This suggests that the company is maintaining a consistent return to unitholders.

Another firm, Delek Logistics Partner LP (DKL), has also raised distribution rates 20 times in the past five years, with a payout ratio of 151%. However, DKL operates in a different segment, focusing on crude and product transportation pipelines and crude oil gathering systems.

Valuation and Return on Equity

Energy Transfer units are trading at a discount relative to the industry. The company’s trailing 12-month Enterprise Value/Earnings before Interest Tax Depreciation and Amortization (EV/EBITDA) is 9.29X, compared to an industry average of 10.65X. This indicates that ET is currently undervalued relative to its peers.

However, the company’s return on equity (ROE) is lower than the industry average. Energy Transfer’s trailing 12-month ROE is 11.08%, compared to an industry average of 13.65%. While this metric reflects how effectively the company uses shareholders’ funds to generate income, it may be a factor for some investors when considering an investment.

Conclusion

Energy Transfer, with over 140,000 miles of pipeline and related infrastructure, is well-positioned to benefit from rising U.S. oil, natural gas, and NGL production. Supported by fee-based earnings and strategic acquisitions, the company is expected to generate sustained value for unitholders.

While the company has a Zacks Rank #3 (Hold), investors who already hold ET can stay invested and enjoy the regular cash distribution. However, due to its lower ROE compared to the industry, some investors may prefer to wait for a more attractive entry point before considering a position.

{kind=link}

Posting Komentar untuk "ET Stock Surpasses Industry Gains: What's the Strategy?"

Posting Komentar