TeraWulf Soars 90% YTD: Buy, Sell, or Hold?

WULF’s Performance in the Second Quarter of 2025

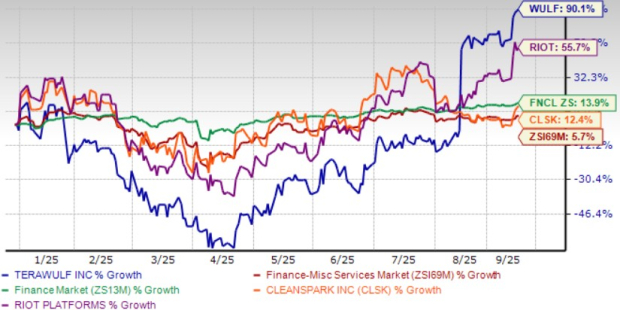

WULF shares have seen a significant increase of 90.1% year to date, although this growth has not matched the performance of the broader Zacks Financial-Miscellaneous Services industry or the Zacks Finance sector. The industry returned 5.2%, while the sector saw a 13.4% gain. TeraWulf, as a vertically integrated owner and operator of next-generation digital infrastructure, reported revenues of $47.6 million in the second quarter of 2025. This represents a 38% sequential increase and a 34% year-over-year rise.

During the same period, WULF self-mined 485 bitcoins at its Lake Mariner facility. The company's bitcoin mining capacity increased by 45.5% year over year, reaching 12.8 EH/s. As of June 30, 2025, TeraWulf owned approximately 70,300 miners, with around 65,100 operational at the facility. However, power costs per bitcoin mined rose by 98.5% year over year due to factors such as the halving event in April, increased network difficulty, and short-term power price volatility. Adjusted EBITDA for the quarter was $14.5 million, down 25.6% from the previous year, compared to a negative $4.7 million in the first quarter of 2025.

Future Outlook and Strategic Moves

Despite these challenges, TeraWulf expects power prices in Upstate New York to remain stable for the rest of 2025. The company anticipates a rate of 5 cents per kilowatt hour for the second half of the year, which could lead to positive contributions from mining operations to EBITDA. However, WULF now projects selling, general, and administrative expenses between $50 million and $55 million, up from the earlier guidance of $40 million to $45 million. This increase is attributed to the accelerated growth of the company’s HPC business.

Expanding Revenue Streams and Strategic Partnerships

TeraWulf is on track to deliver 72.5 MW of HPC colocation capacity under data center lease agreements with Core42 Holding for GPU compute workloads. The WULF Den and CB-1 leases with Core42 are expected to start generating revenue in the third quarter of 2025. Additionally, TeraWulf signed a deal with Fluidstack, an AI cloud platform, to provide more than 360 MW of critical IT load at its Lake Mariner data center. The facility can expand up to 500 MW in the near term and potentially 750 MW with targeted transmission upgrades. At the end of the second quarter, the facility had 245 MW of energized capacity supporting bitcoin mining infrastructure.

This deal is projected to generate $6.7 billion in contracted revenues, with total contract revenues expected to reach $16 billion. Alphabet, through its investment in Fluidstack, is backing the lease obligations, including early termination protections for the first six years. Alphabet also provides $3.2 billion in credit support, increasing its pro forma equity ownership in TeraWulf to approximately 14%.

Expansion and Infrastructure Development

TeraWulf secured a long-term ground lease for approximately 183 acres at the Cayuga site in Lansing, NY. This lease grants the company exclusive rights to develop up to 400 MW of digital infrastructure capacity. It is expected that 138 MW of low-cost, predominantly zero-carbon power will be ready for service in 2026.

Valuation and Market Position

TeraWulf has outperformed peers such as Riot Platforms (RIOT) and Cleanspark (CLSK), whose shares returned 55.7% and 12.4%, respectively, year to date. However, the company faces competition from these firms. Riot Platforms, similar to TeraWulf, is a vertically-integrated bitcoin mining company exploring opportunities for AI and HPC uses. CleanSpark produced 2,012 bitcoins in the third quarter of fiscal 2025, a 28% increase year over year, with average revenue per bitcoin rising 50% to $99,000.

Stock Valuation and Investor Sentiment

WULF shares are currently considered overvalued based on the Value Score of F. In terms of price-to-book ratio, TeraWulf trades at 25.07X, significantly higher than the industry average of 3.67X and the sector average of 4.33X. Compared to Riot Platforms’ 1.78X and Cleanspark’s 1.35X, TeraWulf’s valuation appears premium.

Despite the high valuation, WULF stock is trading above both the 50-day and 200-day moving averages, indicating a bullish trend. However, earnings estimates for 2025 have worsened, with the Zacks Consensus Estimate for TeraWulf’s loss widening by 9 cents to 27 cents per share over the past 30 days. The company reported a loss of 19 cents per share in 2024.

Investment Considerations

Investors should consider the positive developments, such as the lease deals with Fluidstack and Core42, as well as Alphabet’s investment, which could bode well for TeraWulf’s future. However, the stretched valuation and uncertainty around tariffs that affect bitcoin trading add risk. Increasing losses make the WULF stock a risky proposition for new investors.

Currently, TeraWulf holds a Zacks Rank #3 (Hold), suggesting that investors should wait for a more favorable entry point. While the company shows promise, careful evaluation of its financials and market position is essential before making any investment decisions.

{kind=link}

Posting Komentar untuk "TeraWulf Soars 90% YTD: Buy, Sell, or Hold?"

Posting Komentar