Will JD's growing user base drive its next revenue surge?

JD.com's Strategic Growth and Market Position

JD.com has established itself as a key player in China’s e-commerce market through its vertically integrated model. This approach is built on direct procurement, proprietary logistics, and strict quality control. Such a structure provides greater control over inventory and fulfillment compared to pure marketplace platforms. As the Chinese e-commerce market matures, user retention becomes increasingly important for sustainable profitable growth, and this model is expected to remain central.

Expanding User Base and Revenue Trends

JD.com's user base continues to grow steadily. During the third quarter of 2025, quarterly active customers increased by more than 40% year over year. In October, annual active customers surpassed 700 million, and shopping frequency rose by over 40% for the second consecutive quarter. These trends are reshaping revenue composition. Total net revenues grew by 14.9% year over year to RMB 299.1 billion, driven by scaled merchant activity and higher traffic. Broader penetration is expected to continue lifting high-frequency categories that generate steady engagement.

Ecosystem Integration and Technology Investments

Ecosystem integration is reinforcing JD.com’s growth trajectory. JD Food Delivery is creating daily touchpoints that naturally convert into supermarket and general merchandise purchases. Meanwhile, Jingxi extends its reach into lower-tier cities without diluting JD’s core positioning. Offline expansion through JD Mall and JD Appliance City stores supports tactile product categories and improves last-mile reliability. Technology investments in AI search, personalization, and JD Streamer are expected to raise conversion efficiency and reduce merchant-side costs as user activity builds.

Revenue Projections and Challenges

The Zacks Consensus Estimate for JD.com’s 2025 revenues is pegged at $186.3 billion, representing a 15.8% increase year over year. This indicates expectations that user momentum will continue to support revenue acceleration. However, sustaining this trend will require JD.com to navigate rising competition, improve efficiency in new businesses, and adjust to evolving consumer demand. These factors will determine the extent to which user growth can power JD.com’s next phase of revenue expansion.

Intense Competition in the E-commerce Sector

Competition remains intense as JD.com faces off against PDD Holdings and Alibaba. PDD Holdings continues to expand quickly in price-sensitive segments, using Temu’s global reach and aggressive pricing to attract high-volume users. PDD also relies heavily on social commerce loops to sustain engagement. Alibaba is refocusing Taobao and Tmall on efficiency, emphasizing stronger conversion tools and ecosystem coordination. Alibaba is expected to lean more on services and content to retain users. Against both, JD.com’s differentiation comes from fulfillment reliability and merchandise quality, helping it convert and retain users even as PDD and Alibaba compete on scale and price.

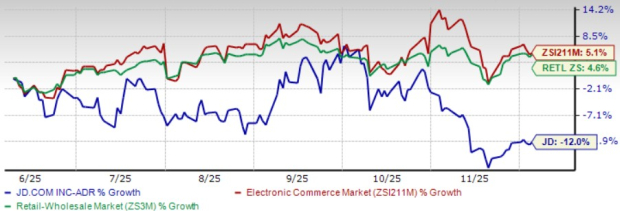

Price Performance and Valuation Analysis

Shares of JD.com have declined by 12% in the past six months, underperforming the Zacks Internet-Commerce industry and Zacks Retail-Wholesale sector’s returns of 5.1% and 4.6%, respectively.

Image Source: Zacks Investment Research

From a valuation standpoint, JD.com is trading at a forward 12-month price-to-earnings ratio of 9.73X, which is lower than the industry average of 24.36X. JD.com carries a Value Score of B.

Image Source: Zacks Investment Research

The Zacks Consensus Estimate for JD.com’s 2025 earnings is pegged at $2.82 per share, up by two cents over the past 30 days. The earnings figure suggests a 33.8% decline year over year.

JD.com, Inc. price-consensus-chart | JD.com, Inc. Quote

JD.com currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

{kind=link}

Posting Komentar untuk "Will JD's growing user base drive its next revenue surge?"

Posting Komentar